Let’s talk micro-investing – the financial world’s equivalent of the sample platter. Apps like Acorns, Stash, and Robinhood have blown open the doors to investing, letting you toss your spare change into the market through round-ups and fractional shares. No more “sorry, you need $1,000 to sit at this table.” Now it’s “hey, got $5? Come on in.”

For most of us – especially if you’re in your 20s or early 30s and your investment knowledge comes from TikTok – these apps feel like a cheat code. Invest without thinking, build wealth while buying coffee, and finally stop getting lectured by your finance-bro friend about “starting early.”

But here’s the thing – these slick interfaces are hiding some uncomfortable truths. While Acorns and its crew have made investing accessible, they’ve also introduced some serious drawbacks that could be quietly sabotaging your financial future.

1. What Is Micro-Investing and Why Has It Become Popular?

Micro-investing is basically investing for people who think they’re too broke to invest. The concept: instead of needing thousands to get started, you can invest literal pocket change. These apps round up your purchases (that $4.25 latte becomes $5, with 75 cents going into investments), let you buy fractions of expensive stocks, and generally make investing feel less like applying for a mortgage and more like ordering DoorDash.

Micro-investing apps are like training wheels – useful to start, but limiting if you never take them off.

The micro-investing landscape is crowded with apps fighting for your spare change: Acorns, Stash, Robinhood, Public, SoFi, and Webull. They’ve attracted millions of first-time investors seeking to build financial literacy and establish investment habits.

The appeal isn’t complicated. When traditional brokerages were giving off “minimum $1,000 to open an account” energy, these apps swooped in with “start with $5” accessibility. For Gen Z and millennials especially, micro-investing hits different with no intimidation factor, automation that actually works, and the psychological win of feeling financially responsible.

2. Financial Limitations and Cost-Related Challenges

Let’s talk about the elephant in the room – these apps aren’t exactly doing this out of the goodness of their hearts. They’ve got to make money somehow, and that “somehow” often comes directly from your pocket in ways that aren’t immediately obvious.

Disproportionate Fee Structures

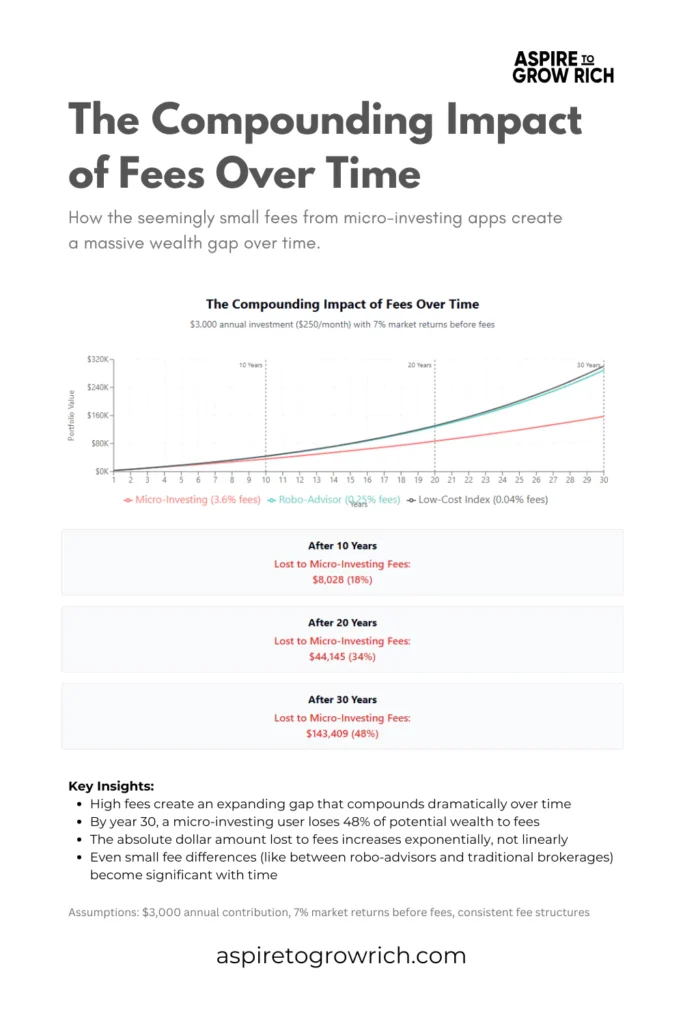

Here’s where micro-investing gets awkward – those “small” fees are actually massive when you look at percentages.

Take Acorns for example which charges you $3 a month. Sounds trivial, right? But do the math: If your portfolio is sitting at $100, you’re paying 3% monthly or 36% annually in fees. For comparison, a wealth management firm charging you 1% would be considered premium pricing.

The $3 monthly fee that seems trivial on paper becomes a 36% annual fee on a $100 portfolio. No investment strategy can overcome that math.

Even at $1,000 invested, you’re still looking at 3.6% annual fees – while traditional brokerages like Fidelity and Schwab are over there charging exactly zero dollars for most ETF trades.

“But they’ve gotta make money somehow!” Sure, but Vanguard manages to offer funds with expense ratios around 0.04% while these apps are effectively charging you 100x that when you’re just getting started.

Look at the actual numbers:

| Platform | Base Fee | On $100 Portfolio (Annual %) | On $1,000 Portfolio (Annual %) |

|---|---|---|---|

| Acorns | $3/month | 36% | 3.6% |

| Stash | $1-9/month | 12-108% | 1.2-10.8% |

| SoFi | $0 but makes money on cash balances | Hidden costs | Hidden costs |

| Fidelity | $0 | 0% | 0% |

That’s not even counting the premium features. Want tax documents that don’t give your accountant a migraine? That’ll be an upgrade. Want actual portfolio rebalancing? Premium tier. These apps turn basic investment features into upsells faster than airlines turned legroom into a luxury.

Overdraft Risks and Budgeting Concerns

The round-up feature – these apps’ claim to fame – has a dark side nobody talks about.

Picture this: You’re having a busy week, swiping your card for coffee, lunch, groceries, gas, repeat. Each purchase gets rounded up. No big deal; it’s just cents, right? Except those round-ups don’t wait for payday – they hit your checking account immediately.

Suddenly, 30 daily transactions mean $15-$20 silently leaving your account right before rent is due. Next thing you know, you’re paying $35 overdraft fees because your micro-investing app was too aggressive with its “painless” saving strategy.

The research doesn’t lie – 68% of Americans live paycheck-to-paycheck at some point in the year. For these folks, random withdrawals with no emergency pause button is a financial accident waiting to happen.

Even worse? Most of these apps don’t have intelligent systems to detect when your balance is getting low. Traditional banks like Chase at least send you warnings when funds are dwindling. Micro-investing apps just keep withdrawing until something bounces.

Limited Growth Potential

If you’re investing $5 daily (which is actually quite aggressive for micro-investing), at a standard 7% annual return, you’ll have about $10,500 after a decade.

That’s… not life-changing money. It won’t fund retirement, buy a house, or even cover a decent used car in most markets. Even if you push it to $10 daily for 30 years, you’re looking at around $116,000 – which sounds impressive until you realize inflation will have cut its purchasing power by more than half.

Meanwhile, traditional retirement accounts like 401(k)s offer employer matches (free money), tax advantages (more free money), and higher contribution limits that actually align with serious financial goals.

The brutal truth is that micro-investing math doesn’t add up for big goals. It’s like trying to fill a swimming pool with a water gun – technically possible, but there are much better tools for the job.

The kicker? Most of these apps don’t even have clear paths to scale up as your income grows. They’re designed around the concept of “investing crumbs” and often lack features that would help you transition to more substantial contributions over time.

E*TRADE, Vanguard, and Fidelity all offer tools to help you calculate your retirement needs and adjust your strategy accordingly. Most micro-investing apps just show you a graph going up and to the right without context about whether that growth will actually meet your needs.

Micro-investing isn’t evil – it’s just dramatically undersized for the job most people need it to do. It’s like bringing a spork to a steakhouse. Sure, it’s better than nothing, but there are more appropriate tools available.

3. Behavioral and Psychological Risks

Ever wonder why Robinhood used to shower you with digital confetti when you made a trade? These apps have gamified investing to an almost dangerous degree. The dopamine hit from making a quick trade is real, and it’s addictive.

Research shows active traders underperform passive investors by a staggering 6.5% annually on average. A 2023 study found that micro-investing app users trade 5x more frequently than traditional brokerage clients, with 63% of users making at least one trade weekly. That’s not investing – that’s just gambling with extra steps.

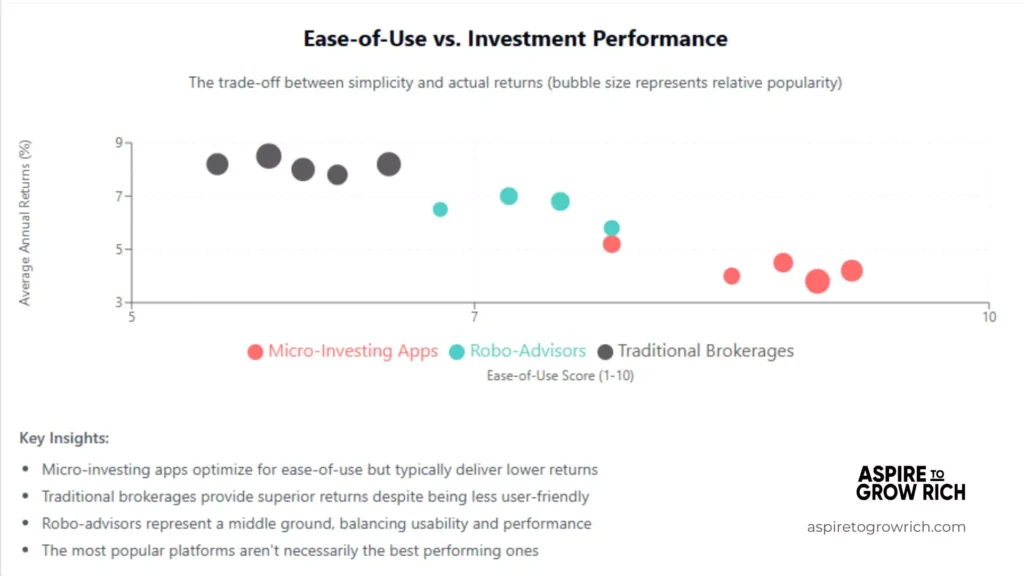

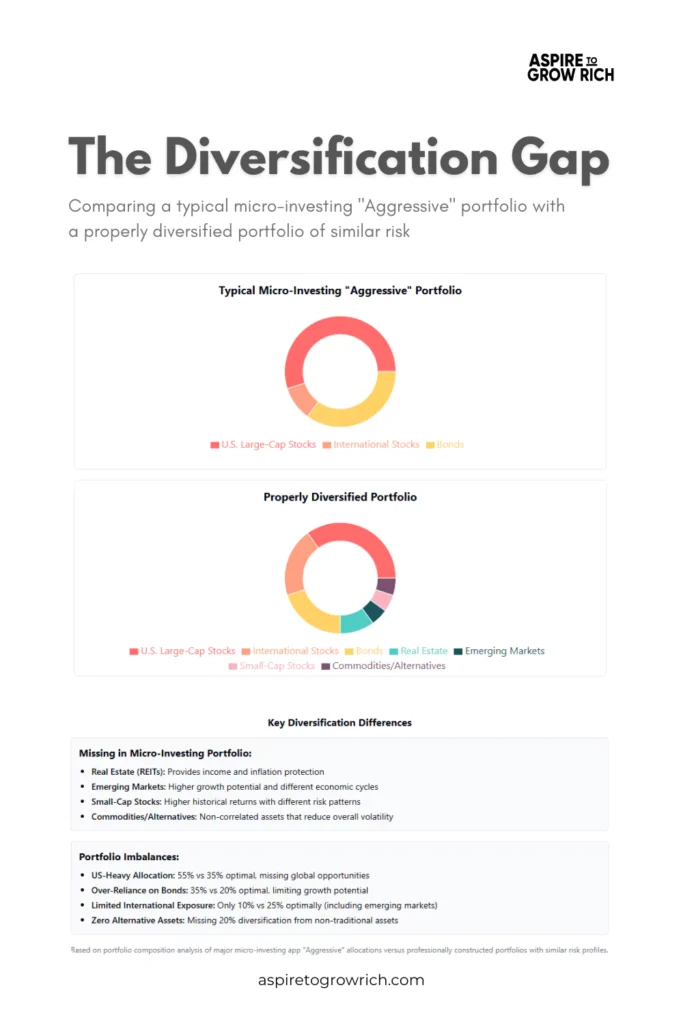

“Conservative,” “Moderate,” or “Aggressive” – these oversimplified portfolio options reduce complex financial decisions to something barely more nuanced than “small, medium, or large.” What’s worse, these labels often hide portfolios that don’t match what you might expect. Take Acorns’ “Aggressive” portfolio – it contains 55% large-cap U.S. stocks, 10% international stocks, and a whopping 35% in bonds. Any financial advisor would call that moderate at best.

This oversimplification creates dangerous knowledge gaps where you don’t learn about asset allocation, don’t understand how fees impact returns, and don’t grasp how different assets perform in various economic conditions.

4. Technical and Operational Drawbacks

Remember when Robinhood went completely dark during the 2020 meme stock frenzy? User reviews consistently flag reliability issues across these platforms: 18% of Webull users reported app crashes or delayed order execution in 2024, Public.com faced criticism for slow fund withdrawals, and Stash regularly experiences synchronization issues between bank accounts and investment portfolios.

When traditional brokerages like Fidelity or Charles Schwab have outages (which is rare), they typically have backup phone systems where you can still execute trades. Try calling most micro-investing apps during an outage – if they even have a phone number, you’ll likely reach an AI chatbot or a customer service rep with limited capabilities.

As soon as you develop any real investment knowledge, you’ll hit the ceiling on what these platforms can do: only 12% of micro-investing platforms offer advanced charting capabilities, fewer than 5% provide backtesting tools, and almost none give access to SEC filings, earnings reports, or analyst recommendations.

5. Investment Strategy Shortcomings

Stash brags about offering “thousands of investment options,” but in reality, you’re looking at about 200 ETFs – a tiny fraction of the 3,000+ ETFs available through traditional brokerages. The international exposure on these platforms is particularly sad with most portfolios allocating less than 15% to international markets, despite global stocks making up more than 40% of investment opportunities worldwide.

A proper investment strategy isn’t about how easy it is to use the app – it’s about how effectively it builds wealth over decades.

For platforms like Robinhood and Webull that let you pick individual stocks, the lack of diversification gets even worse. A 2023 study found that 63% of micro-investing app users hold fewer than five stocks, with a shocking 28% having their entire portfolio in a single company.

Remember Tesla’s 65% nosedive in 2022? Users who were overexposed to tech darlings watched their portfolios get demolished. Meanwhile, boring, diversified portfolios at traditional brokerages weathered the storm much better.

6. Educational and Informational Gaps

A review of 15 micro-investing platforms found that 73% provided zero material on fundamental analysis, and a whopping 89% completely ignored tax strategies. Robinhood’s much-touted “Learn” section covers just 12 basic topics written at a middle-school reading level. For comparison, Fidelity offers over 300 articles, interactive calculators, webinars, and detailed case studies.

Want real-time data to make informed decisions? That’ll cost you extra – if it’s available at all. Public.com serves up delayed quotes unless you pay for premium access, while Stash doesn’t even offer earnings calendars or analyst ratings. Without proper tools to contextualize market movements, users end up making decisions based on headlines, social media noise, or—worst of all—Reddit threads.

7. Tax Implications and Management Challenges

Tax-loss harvesting (selling losing investments to offset gains) is completely absent from 95% of micro-investing platforms. It’s a standard feature in grown-up investing tools like Wealthfront, where it saves users an average of $1,200 annually in tax bills.

If you’re making 30 purchases daily (not uncommon with round-up features), you’ll generate 150-200 monthly micro-investments. That’s over 2,400 separate line items annually that could potentially appear on your tax documents. According to survey data, 68% of users report significant difficulty distinguishing between taxable events and non-reportable transfers when tax season hits.

Even worse, many of these platforms charge extra for decent tax documentation, with comprehensive documents locked behind premium tiers.

8. Better Alternatives to Consider

Fidelity, Charles Schwab, and Vanguard all offer accounts with zero minimum balance requirements now. Zero. As in, the same amount you need for Acorns or Stash, but without the $3 monthly subscription fee eating your returns.

A simple three-fund portfolio with total US market, international market, and bond index funds gives you more diversification than 90% of micro-investing portfolios. The best part? You can build this with expense ratios under 0.1% – a fraction of what you’re paying with micro-apps when you factor in their subscription fees.

If your workplace offers a 401(k), especially with matching contributions, and you’re not maxing that match before using micro-investing apps, you’re literally leaving free money on the table. A typical employer match is 50-100% of your contributions up to a certain percentage of your salary – an instant 50-100% return on your investment before a single market movement happens.

For those who like automation, proper robo-advisors like Betterment and Wealthfront charge 0.25% annually – which sounds higher than the “free” trading on micro-apps until you do the math. On a $1,000 account, that’s $2.50 per year versus $36 in Acorns subscription fees.

9. Who Might Still Benefit from Micro-Investing Apps?

If your current investment strategy is “hope my checking account has money left at the end of the month,” micro-investing might help you establish saving habits. For people who’ve never saved a dime, the psychological trick of automated round-ups can be genuinely useful – just remember this is a starting point, not a destination.

For those working minimum wage who can only spare $5-10 weekly, the fractional shares feature means someone can own a piece of companies they recognize, even with just a few dollars to invest. Is paying $3 monthly on a tiny portfolio ideal? No, but it might be worth it for the accessibility factor – at least temporarily.

Some financially savvy people use micro-investing apps alongside traditional investment accounts for specialized “fun money” accounts or specific short-term goals while keeping their serious long-term investments elsewhere.

Wrapping Up

Micro-investing apps solved one problem brilliantly – getting people started with tiny amounts of money. But they’ve created a host of other issues that can seriously damage your long-term financial health. The biggest danger isn’t even the direct costs – it’s the opportunity cost of thinking you’re properly investing when you’re stuck in financial kindergarten.

Whether you’re currently using micro-investing apps or considering them, here’s your game plan:

- Cap your fees at 0.5% or less of your portfolio annually

- Either build your balance to where fees become reasonable ($10,000+ for a $3 monthly fee) or switch platforms

- Supplement your financial education beyond what apps provide

- Free resources like Investor.gov, Khan Academy, and the Bogleheads forum offer no-nonsense education

- Diversify across platforms based on strengths

- Use employer 401(k)s for matching contributions and tax advantages (always max this first!)

- Consider traditional brokerages for your core investment portfolio

- Monitor and modify your investing behavior

- Disable push notifications that encourage frequent checking and trading

- Set monthly limits on how often you can make changes to your portfolio

The bottom line is that micro-investing apps are like those first bikes with training wheels – perfectly fine to start with, but you’ll look ridiculous still using them at 30. Real wealth-building isn’t about confetti animations and social feeds – it’s about consistent contributions, proper diversification, minimizing costs, and letting compound interest work its magic over decades.