Are you looking to start investing but think you need thousands to begin? Think again. Welcome to your comprehensive guide to micro-investing, the revolutionary way young adults are building wealth $5 at a time.

Have you ever caught yourself thinking “I’ll start investing when I have more money”? You’re not alone. 67% of young adults believe they need at least $1,000 to start investing. Here’s the game-changing truth: with micro-investing, you can start building your investment portfolio with just your spare change.

What You’ll Learn in This Guide

Micro-investing has transformed how Gen Z and millennials approach wealth building. Whether you’re a college student, young professional, or side hustle entrepreneur, this comprehensive guide will show you exactly how to start your investment journey – no finance degree required.

In this updated 2025 guide, we’ll cover:

- How to start investing with as little as $5

- Step-by-step guidance for choosing the right investment apps

- Smart strategies for automated investing

- Real examples of successful young investors

- Tax-smart investing approaches for beginners

- Tips for growing your small investments into significant wealth

Gone are the days when investing was exclusive to Wall Street experts. Today’s digital investment platforms and automated investing tools have democratized wealth building. Through features like round-up investments and recurring deposits, you can start growing your money while barely noticing the amounts you’re setting aside.

Maybe you’re wondering if micro-investing is really worth your time. Consider this: if you invested just $5 daily through round-ups and automated deposits, with an average market return, you could accumulate over $28,000 in ten years. That’s the power of starting small and staying consistent.

Ready to take control of your financial future? Let’s dive into everything you need to know about micro-investing, from choosing your first investment app to building a smart, diversified portfolio that grows with you.

Understanding Micro-Investing

Think of micro-investing as your personal wealth-building escalator – it’s an easier way up than taking the stairs all at once. Instead of waiting until you have hundreds or thousands to invest, micro-investing platforms let you start your investment journey with amounts as small as the change from your morning coffee.

Breaking Down Micro-Investing in Simple Terms

At its core, micro-investing is exactly what it sounds like: investing in tiny amounts. But what makes it truly powerful is how it combines three key elements that are perfect for young investors:

- Fractional Shares: Remember when buying a single share of Amazon would cost over $3,000? With fractional shares, you can own a slice of premium stocks with just a few dollars. This means you can build a diversified investment portfolio even with small amounts.

- Automated Investing: Think of this as your financial autopilot. Modern micro-investing platforms can automatically invest your spare change, recurring deposits, or both. When you buy that $3.50 latte, these apps can round up to $4.00 and invest the $0.50 difference without you lifting a finger.

- Smart Portfolio Building: Most micro-investing apps don’t just hold your money – they invest it in diversified ETF portfolios. These are pre-built collections of stocks and bonds that help spread your risk, even with small investment amounts.

Why Micro-Investing Makes Sense for Young Adults

Let’s be honest – as a young adult, you’re juggling a lot. Between student loans, rent, and trying to have a social life, saving large amounts for investing might feel impossible. This is where micro-investing shines:

- Low Entry Barrier: Start with literally your spare change

- Learn While You Earn: Gain real investing experience without risking large amounts

- Flexibility: Increase or decrease your investment amounts as your budget allows

- Time Advantage: Start early and let compound interest work its magic

The Science Behind Small Investments

Here’s a reality check that might surprise you: investing just $1.50 daily (the average round-up amount for most users) can grow to over $10,000 in ten years, assuming average market returns. This isn’t get-rich-quick math – it’s the power of consistent micro-investing combined with compound interest.

Common Micro-Investing Methods

Let’s look at the most popular ways young investors are using micro-investing platforms:

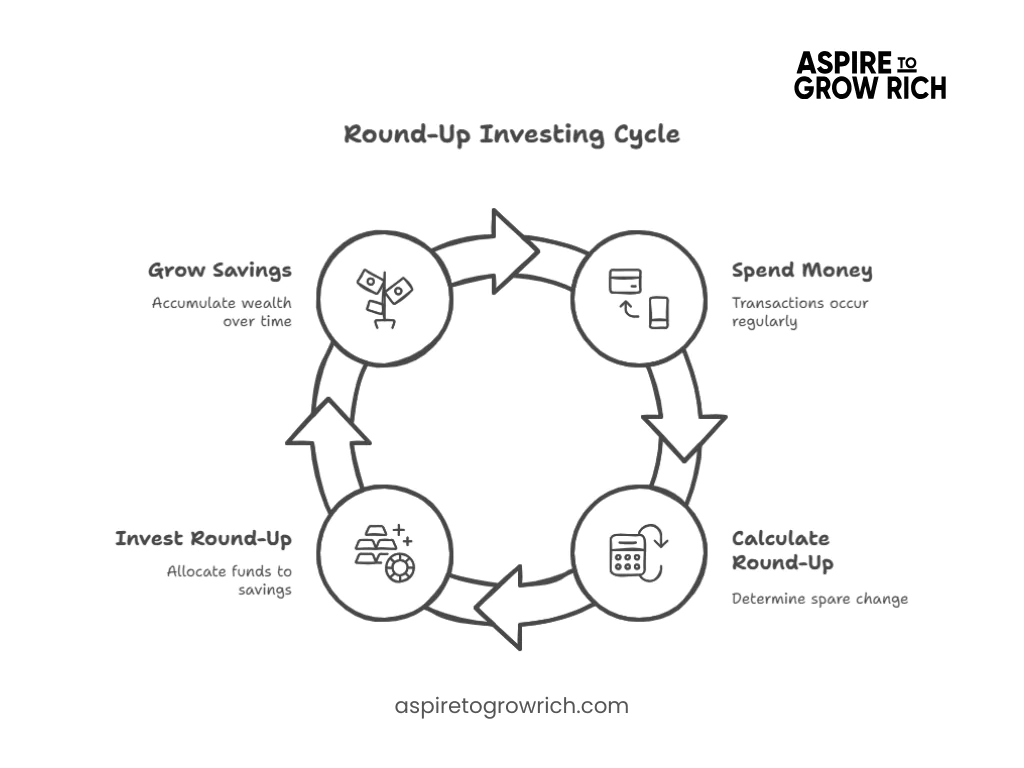

Round-Up Investing Every time you make a purchase, the amount is rounded up to the nearest dollar, and the difference is invested. It’s like a digital change jar that grows your wealth.

Regular Small Deposits Set up automatic weekly or monthly deposits, even if it’s just $5 or $10. This creates a consistent investing habit without straining your budget.

Earned Cash Back Some platforms offer cash back on purchases from partner retailers, automatically investing these rewards into your portfolio.

Getting Started with $5

Ready to turn that coffee money into an investment portfolio? Let’s break down exactly how to start your micro-investing journey, no financial jargon is required.

Getting Started Is Easier Than You Think

Remember when opening an investment account meant visiting a stuffy bank office with a stack of paperwork? Those days are gone. Modern micro-investing platforms have streamlined the process down to a few simple steps you can complete right from your phone.

Step 1: Choose Your First Micro-Investing Platform

Before you invest your first $5, you’ll need to pick a platform. Here’s what to look for:

- Minimum Investment Requirements: Some apps let you start with just $1, while others might need $5

- Monthly Fees: Look for platforms with low or no fees for small balances

- Investment Options: Make sure the platform offers ETFs or other diversified investment options

- User Interface: Choose an app that feels intuitive and easy to understand

- Security Features: Verify the platform has strong encryption and SIPC insurance protection

Step 2: Setting Up Your Account (The 10-Minute Process)

Here’s exactly what you’ll need to get started:

- A valid government ID

- Your social security number

- A linked bank account

- About 10 minutes of free time

Most platforms will instantly verify your identity, letting you start investing immediately.

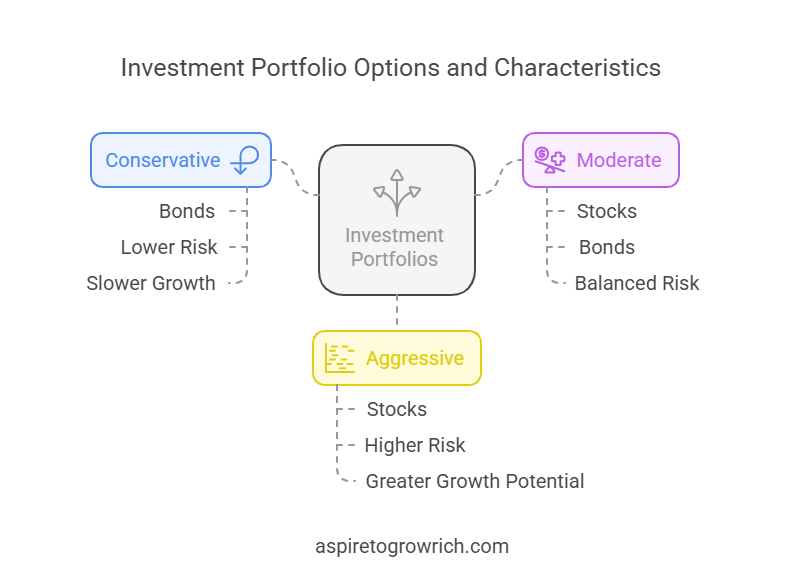

When you make your first deposit, you’ll typically choose between several investment portfolios. These usually range from:

🚨 Pro Tip

As a young investor, you generally have time to recover from market ups and downs, so don’t be afraid to consider more aggressive growth options.

Making Your First Investment

Let’s walk through a real example of starting with $5:

- Initial Deposit: Transfer your first $5 from your linked bank account

- Choose Your Portfolio: Select an investment strategy that matches your goals

- Set Up Automation: Configure round-ups or recurring deposits

- Monitor Your Progress: Watch your tiny investments start working for you

Understanding the Fees (Don’t Let Them Eat Your Returns)

Before you get started, understand the common fees you might encounter:

- Monthly Service Fees: Usually $1-3 per month

- Management Fees: Often 0.25% to 0.50% annually

- ETF Fees: Additional small fees from the funds themselves

📱 Smart Move

Many platforms waive monthly fees for students or offer free periods for new users. Take advantage of these offers!

Your First Week of Micro-Investing

Here’s what to expect in your first week:

Comparing the Best Micro-Investing Platforms (2025 Edition)

Not all micro-investing platforms are created equal. Let’s cut through the marketing hype and break down what each popular platform offers for young investors in 2025.

Top Micro-Investing Platforms at a Glance

Acorns

Best for: Automated round-up investing

- Minimum Investment: $5

- Monthly Fee: $3-5

- Standout Features:

- Automatic round-ups from linked cards

- Found money® program with cash-back rewards

- Built-in retirement accounts (IRA options)

- Banking integration with Metal debit card

💡 Real User Insight: Most young investors report saving an average of $30-50 monthly through round-ups alone on Acorns.

Stash

Best for: Learning while investing

- Minimum Investment: $5

- Monthly Fee: $1-9

- Standout Features:

- Stock-back® rewards on purchases

- Fractional shares of individual stocks

- Educational content and guidance

- Customizable portfolio options

Robinhood

Best for: Active micro-traders

- Minimum Investment: $1

- Monthly Fee: $0

- Standout Features:

- Commission-free trading

- Cryptocurrency access

- Instant deposit availability

- Advanced trading tools

Feature-by-Feature Comparison

Security Features

- Acorns: 256-bit encryption, SIPC insurance

- Stash: Biometric authentication, SIPC protection

- Robinhood: Two-factor authentication, fraud protection

Investment Options

- Acorns: ETF portfolios only

- Stash: ETFs, individual stocks, crypto

- Robinhood: Stocks, ETFs, options, crypto

Automated Features

| Feature | Acorns | Stash | Robinhood |

|---|---|---|---|

| Round-Ups | ✅ | ✅ | ❌ |

| Recurring Deposits | ✅ | ✅ | ✅ |

| Portfolio Rebalancing | ✅ | ✅ | ❌ |

| Smart Deposits | ✅ | ✅ | ❌ |

Choosing the Right Platform for Your Goals

For Complete Beginners

If you’re new to investing and want a hands-off approach, Acorns is your best bet. The platform’s automated features and simple interface make it perfect for building good investing habits.

For Active Learners

Stash offers the best educational resources and allows you to gradually take more control of your investments as you learn. Their stock-back® program also helps you learn about investing through your everyday purchases.

For Future Day Traders

If you want to learn active trading while starting small, Robinhood’s commission-free structure and user-friendly interface make it an excellent choice.

Hidden Fees to Watch Out For

Every platform has its costs. Here’s what to consider beyond the monthly fees:

- ETF Expense Ratios: 0.03% to 0.25% annually

- Account Transfer Fees: Usually $75-100

- Foreign Transaction Fees: Varies by platform

- Account Closure Fees: Some platforms charge $50-75

Making Your Decision

Consider these factors when choosing your platform:

- Investment Style: Do you prefer hands-off or active management?

- Budget: Can you commit to monthly fees?

- Features: Which automated tools matter most to you?

- Growth Plans: Will the platform scale with your needs?

Smart Micro-Investing Strategies for Young Adults

You’ve got your platform picked out and you’re ready to start investing. Now let’s make sure your money works as intelligently as possible with proven strategies that fit a young adult’s lifestyle.

Round-Up Investing: The Stealth Wealth Strategy

Think of round-ups as your invisible savings plan. Here’s how to maximize them:

Optimizing Your Round-Ups

- Link multiple cards to capture more round-up opportunities

- Use your card for small purchases ($1-15 range) to generate more round-ups

- Consider “2x” or “3x” round-up multipliers for accelerated growth

Pro Strategy

Use your card for small purchases like coffee or snacks. A $3.50 coffee rounds up to $4.00, investing $0.50 each time. Do this daily, and you’re investing $15 monthly without thinking about it.

Setting Up Smart Recurring Investments

The “Paycheck Partition” Method

- Start with just 1% of your paycheck

- Increase by 0.5% every three months

- Set up automatic transfers on payday

- Aim to reach 10-15% over time

💡 Strategy Spotlight

If you make $3,000 monthly, starting at 1% means $30/month. By year’s end, you could comfortably invest $90-120 monthly through gradual increases.

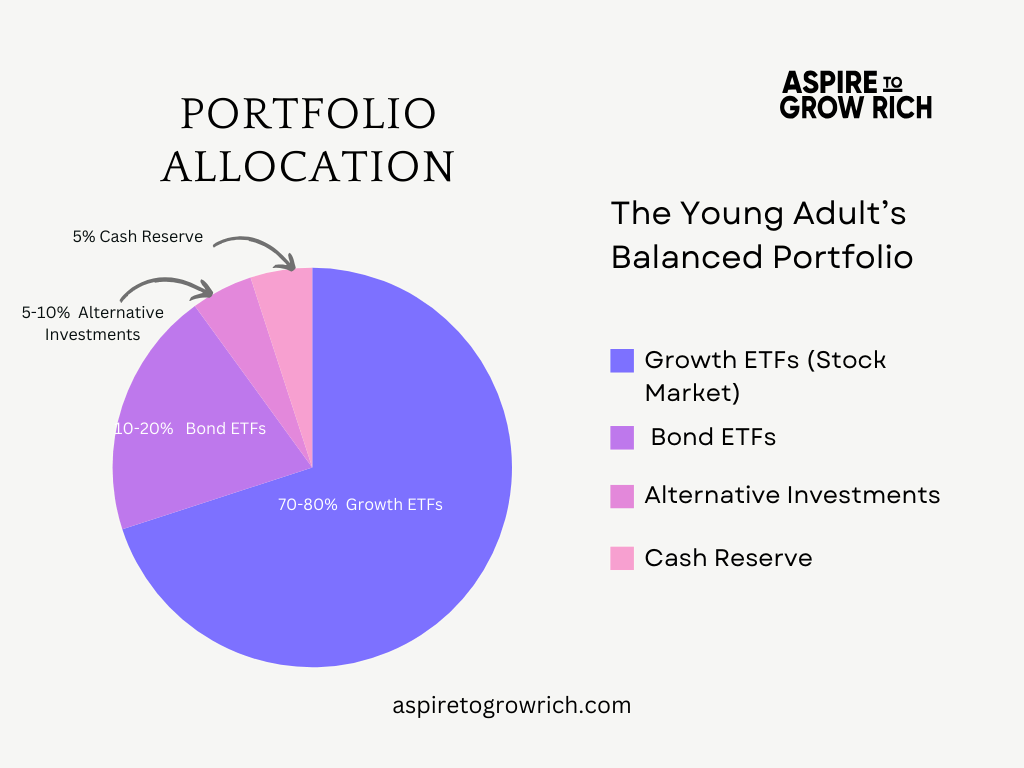

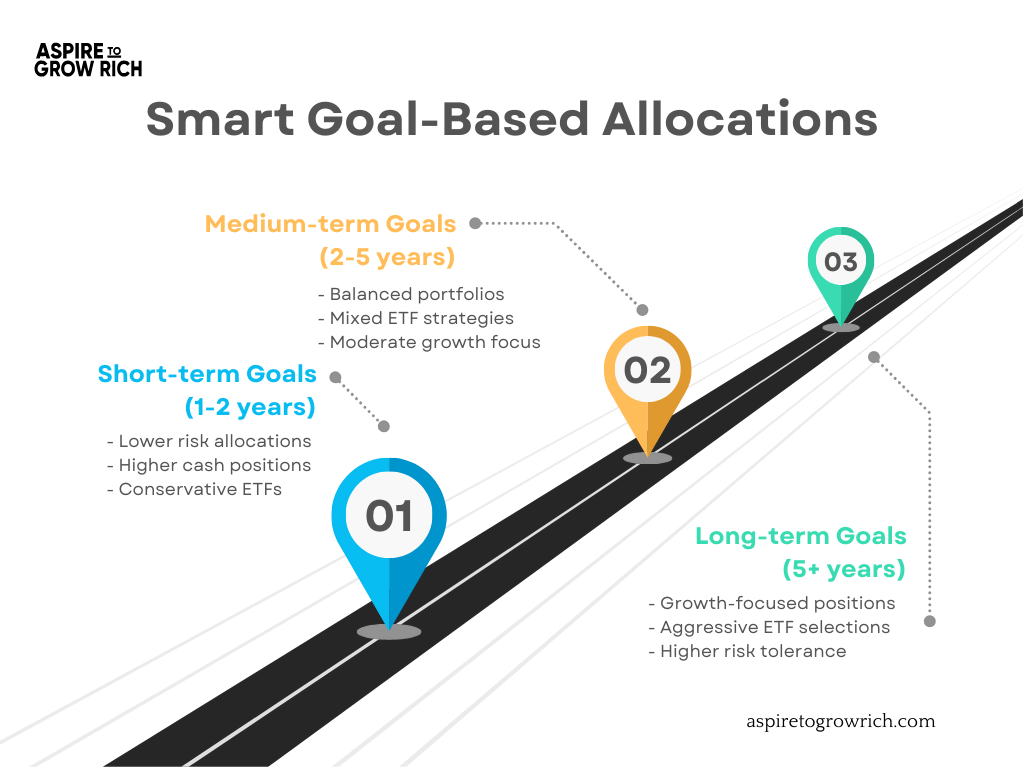

Suggested Portfolio Allocation for Gen Z

The Young Adult’s Balanced Portfolio

- 70-80% Growth ETFs (Stock Market)

- 10-20% Bond ETFs

- 5-10% Alternative Investments

- 5% Cash Reserve

Risk Management Tip

Being young means you can afford to be aggressive, but never invest money you’ll need in the next 12 months.

Tax-Efficient Micro-Investing Approaches

Smart Tax Strategies for Small Investors

- Hold Investments Long-Term

- Keep investments for over a year when possible

- Take advantage of lower long-term capital gains rates

- Use Tax-Advantaged Accounts

- Consider a Roth IRA for some of your micro-investments

- Take advantage of tax-free growth potential

- Track Your Investments

- Keep records of all deposits and round-ups

- Monitor your gains and losses for tax season

Dollar-Cost Averaging: Your Best Friend

This strategy means investing the same amount regularly, regardless of market conditions. Here’s why it works especially well with micro-investing:

- Reduces the impact of market volatility

- Removes emotional decision-making

- Works perfectly with automated deposits

- Builds consistent investing habits

Example DCA Strategy:

Weekly Investment: $10

Monthly Round-ups: ~$20

Quarterly Bonus: $50

Annual Total: ~$800

Advanced Features to Maximize Your Returns

Now that you’ve mastered the basics, let’s explore the advanced features that can take your micro-investing strategy from good to great. These tools and techniques can help optimize your returns without requiring hours of portfolio management.

Portfolio Rebalancing: Keeping Your Investments on Track

Think of rebalancing like tuning a car – it keeps everything running at peak performance.

Automatic vs. Manual Rebalancing

Most micro-investing platforms offer automatic rebalancing, but understanding the process helps you make smarter decisions:

- Drift Monitoring: Your portfolio naturally shifts from its target allocation

- Threshold Triggers: Rebalancing occurs when allocations drift by 5% or more

- Tax-Smart Timing: Platforms typically rebalance during natural cash flows to minimize tax impact

🔄 Pro Tip

Check if your platform charges for manual rebalancing. Most offer it free, but some may count it as a trade.

Dividend Reinvestment: The Compound Effect

How DRIP Works in Micro-Investing

- Automatically reinvests earned dividends

- Purchases fractional shares with any amount

- Compounds return over time

- Reduces cash drag on your portfolio

Example:

Initial Investment: $100

Monthly Addition: $50

Dividend Yield: 2%

With DRIP (10 years): $7,839

Without DRIP (10 years): $7,147

Difference: $692 (9.7% more)

Smart Auto-Deposit Strategies

Advanced Deposit Rules

- Threshold-Based Deposits

- Set minimum bank balance requirements

- Automatically pause when funds are low

- Resume when balance recovers

- Smart Scheduling

- Align with paycheck dates

- Schedule around bill payments

- Adjust for seasonal income changes

- Dynamic Deposit Scaling

- Increase deposits with income growth

- Adjust for bonus payments

- Scale with spending patterns

Investment Tracking Tools

Essential Metrics to Monitor

- Rate of Return

- Overall portfolio performance

- Individual investment returns

- Comparison to benchmarks

- Cost Basis Tracking

- Purchase prices

- Reinvested dividends

- Fee impacts

- Risk Metrics

- Volatility measures

- Diversification scores

- Risk-adjusted returns

Advanced Risk Management Techniques

Building Safety Nets

- Emergency Fund Integration

- Keep 3-6 months of expenses liquid

- Use high-yield savings alongside investments

- Set up smart withdrawal rules

- Investment Laddering

- Stagger investment timing

- Diversify across entry points

- Reduce market timing risk

Smart Goal-Based Allocations

Micro-Investing Strategy with Examples

There’s nothing quite like learning from real experiences. Let’s dive into actual micro-investing journeys from young adults who’ve successfully built their wealth through small, consistent investments.

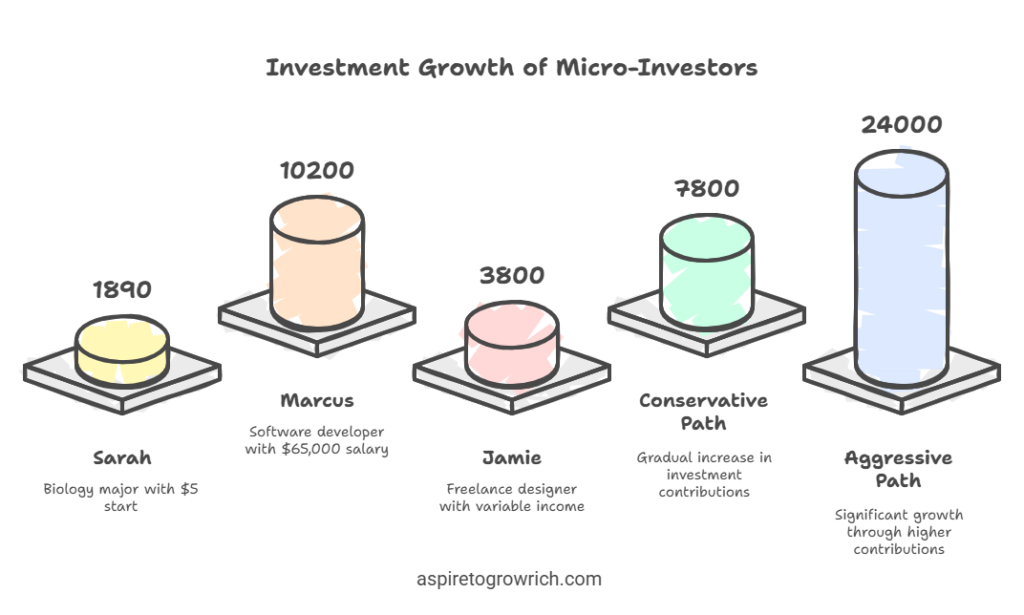

The College Student’s Strategic Saving

Sarah, a 21-year-old biology major, didn’t wait for a six-figure salary to start investing—she started with $5. She rounded up spare change, cut back on coffee, and invested $65/month from her part-time job. Two years later, she had $1,890, a solid grasp of market basics, and a plan to invest more after graduation. The lesson? Small, consistent moves add up.

After 2 Years:

- Total Invested: $1,560

- Portfolio Value: $1,890

- Learned: Market basics, compound interest

- Next Step: Increasing contributions post-graduation

💡 Key Takeaway: “I never missed the round-up money, but it added up faster than I expected.”

The Young Professional’s Growth Plan

Meet Marcus, 25, a software developer who turned spare change into serious wealth.

He started small—$100, rounding up purchases, auto-investing $200/month, and tossing in 25% of bonuses. Three years later? $8,400 invested, now worth $10,200.

Along the way, he mastered diversification and tax hacks also even maxed out his Roth IRA. His Small moves make a big impact. 🚀

After 3 Years:

- Total Invested: $8,400

- Portfolio Value: $10,200

- Learned: Portfolio diversification, tax strategies

- Achievement: Maxed out Roth IRA through micro-investing

The Side Hustler’s Success

Meet Jamie, a 23-year-old freelance designer with an unpredictable income. Investing felt overwhelming, so he started small—just $10. His rule? Invest 5% of every payment, round up expenses, and give himself a “bonus” every quarter.

18 months later: $3,200 invested, now worth $3,800. More than money, he learned to manage his business better. Oh, and those investment fees? Tax write-offs. Turns out, small moves add up—just like his designs, every detail counts.

After 18 Months:

- Total Invested: $3,200

- Portfolio Value: $3,800

- Business Growth: Used investment knowledge to better manage business finances

- Added Benefit: Tax deductions from investment fees

Five-Year Growth Scenario

Based on combined data from successful micro-investors:

Conservative Path

| Year | Amount |

|---|---|

| Year 1 | $50/month ($600) |

| Year 2 | $75/month ($900 |

| Year 3 | $100/month ($1,200) |

| Year 4 | $150/month ($1,800) |

| Year 5 | $200/month ($2,400) |

| Total Invested | $6,900 |

| Potential Value | $7,800-$8,500 |

Aggressive Path

| Year | Amount |

|---|---|

| Year 1 | $100/month ($1,200) |

| Year 2 | $200/month ($2,400) |

| Year 3 | $300/month ($3,600) |

| Year 4 | $400/month ($4,800 |

| Year 5 | $500/month ($6,000) |

| Total Invested | $18,000 |

| Potential Value | $21,000-$24,000 |

Sarah rounded up spare change, Marcus automated his deposits, and Jamie treated investing like a side hustle. None of them started big, but time and habit did the heavy lifting. Micro-investing isn’t about getting rich fast—it’s about getting started and letting compounding do its thing.

Common Pitfalls These Investors Avoided

- The Checking Obsession

- Successful investors checked monthly, not daily

- Focused on long-term trends

- Avoided emotional decisions

- The All-In Mistake

- Kept emergency funds separate

- Balanced investing with debt payments

- Maintained realistic contribution levels

- The Platform Hop

- Stuck with the chosen platform

- Focused on strategy, not tools

- Minimized transfer fees

Tax Implications and Legal Considerations

Let’s demystify the tax side of micro-investing. While it might seem complicated, understanding these basics will help you keep more of your returns and stay compliant with tax laws.

Tax Reporting Basics for Micro-Investors

What You’ll Need to Report

Every micro-investment platform will send you tax forms, typically:

- Form 1099-B: Shows your gains and losses

- Form 1099-DIV: Reports dividend payments

- Form 1099-INT: Details interest earned

Important Dates:

- Forms available: January 31st

- Tax filing deadline: April 15th

- Extension deadline: October 15th

Understanding Capital Gains

Short-Term vs. Long-Term Gains

Short-Term (Held Less than 1 year):

– Taxed as regular income

– Higher tax rates apply

– Ranges from 10% to 37%

Long-Term (Held Greater than 1 year):

– Preferential tax rates

– Usually 0%, 15%, or 20%

– Based on income bracket

💡 Tax-Smart Strategy: Hold investments for at least one year when possible to qualify for lower long-term capital gains rates.

Record-Keeping Requirements

Essential Records to Maintain

- Investment Purchases

- Date of purchase

- Amount invested

- Fees paid

- Platform used

- Investment Sales

- Sale date

- Amount received

- Fees incurred

- Gain/loss calculation

- Dividend and Interest

- Payment dates

- Amount received

- Reinvestment details

- Type of dividend

Year-End Tax Strategies

Smart Moves to Consider

- Tax Loss Harvesting

- Sell underperforming investments

- Offset gains with losses

- Reinvest in similar (not identical) assets

- Limit wash sales

- Dividend Planning

- Check ex-dividend dates

- Plan purchases around distributions

- Consider tax-efficient funds

- Contribution Timing

- Max out tax-advantaged accounts

- Consider year-end lump sums

- Plan for tax year deadlines

Working with Tax Professionals

When to Seek Help

- Multiple investment platforms

- Large gains or losses

- Complex tax situation

- First-time investor

Finding the Right Help

Options to Consider:

1. Tax Software: For simple situations

2. Online Tax Services: Moderate complexity

3. CPA: Complex situations

4. Financial Advisor: Ongoing planning

Special Considerations

State Tax Implications

- State tax rates vary

- Some states have no capital gains tax

- Check local requirements

Alternative Minimum Tax (AMT)

- This may apply to higher earners

- Can affect investment strategy

- Requires additional planning

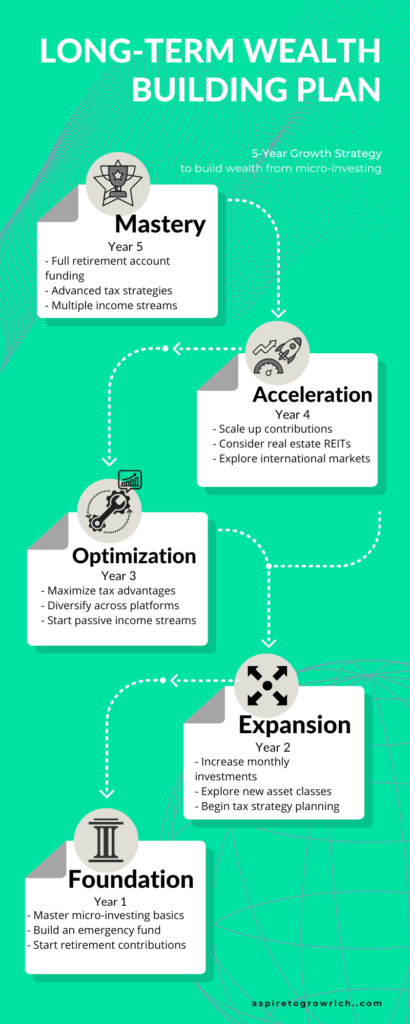

Scaling Up: Growing Your Micro-Investments Over Time

Moving from micro to macro isn’t just about investing more money – it’s about evolving your strategy as your wealth and knowledge grow. Let’s explore how to scale your investments intelligently.

When to Increase Your Contributions

Financial Milestones That Signal It’s Time to Scale Up

- Income Increases

- After a raise (commit 50% of the increase)

- Bonus payments

- Side hustle revenue

- Debt payoff completion

- Expense Decreases

- Finished paying student loans

- Reduced living costs

- Eliminated subscription services

- Refinanced high-interest debt

Scaling Strategy Example:

Base Salary: $50,000

Raise Amount: $5,000

Current Investment: $100/month

New Investment: $300/month

($100 base + $200 from raise)

Portfolio Diversification Strategies

Building a More Sophisticated Portfolio

Starting Portfolio:

– 90% Broad Market ETFs

– 10% Bonds

Intermediate Portfolio:

– 65% US Stocks

– 15% International Stocks

– 15% Bonds

– 5% Real Estate ETFs

Advanced Portfolio:

– 50% US Stocks

– 20% International Stocks

– 15% Bonds

– 10% Real Estate

– 5% Alternative Investments

Transitioning to Larger Investments

Beyond Micro-Investing Platforms

- Robo-Advisor Services

- More sophisticated algorithms

- Tax-loss harvesting

- Custom portfolio options

- Traditional Brokerages

- Full-service options

- Research tools

- Advanced trading capabilities

- Retirement Accounts

- 401(k) maximization

- IRA contributions

- HSA investments

Setting Realistic Growth Targets

Milestone-Based Goals

- First $10,000

- Focus on consistent contributions

- Learn market basics

- Build good habits

- $25,000 Portfolio

- Increase diversification

- Consider professional advice

- Review tax strategies

- $50,000+ Portfolio

- Advanced investment options

- Estate planning basics

- Risk management review

Final Tips for Scaling Success

Key Points to Remember

- Stay Consistent

- Don’t abandon proven strategies

- Keep automated investments

- Maintain emergency fund

- Manage Risk

- Increase diversification with growth

- Regular portfolio reviews

- Maintain long-term perspective

- Continue Learning

- Follow market trends

- Study investment strategies

- Network with other investors

Wrapping Up

Looking back at everything we’ve covered, it’s clear that micro-investing isn’t just about small contributions – it’s about building a foundation for long-term financial success. Whether you’re a college student starting with spare change or a young professional ready to scale up, the principles we’ve discussed can help transform your financial future.

Key Takeaways from This Guide

Remember that successful micro-investing comes down to a few core principles:

- Start small, but start now

- Stay consistent with your investments

- Use automation to your advantage

- Keep learning and adjusting your strategy

- Scale up when you’re ready

Your Next Steps: Taking Action

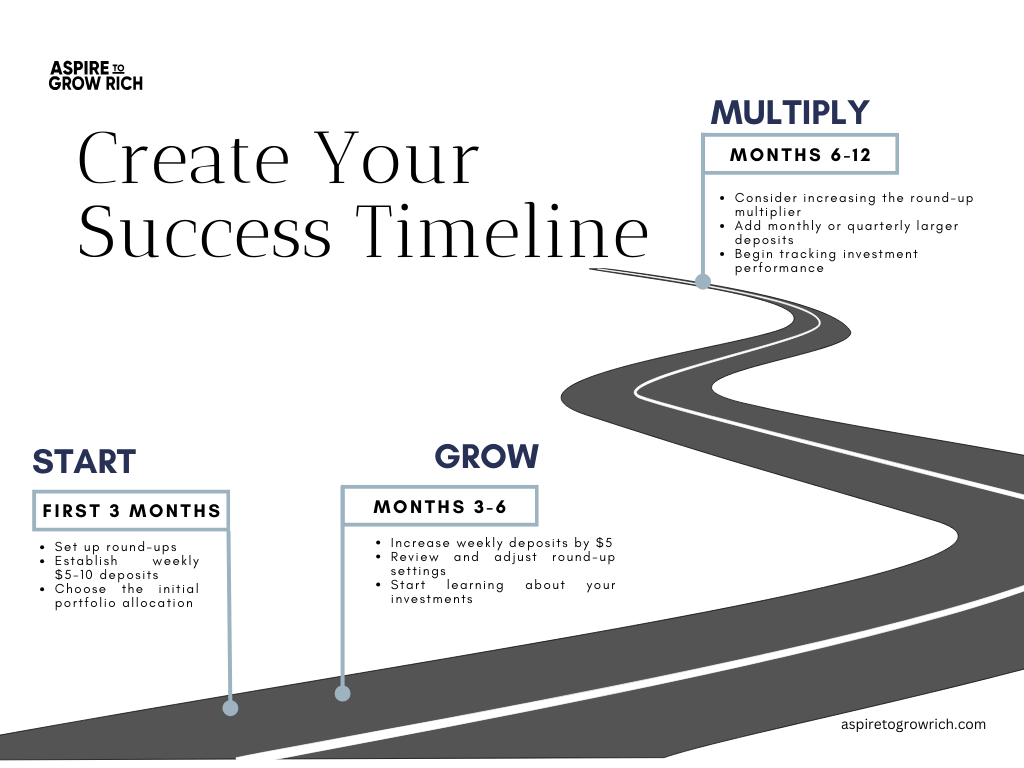

Immediate Actions (Next 24 Hours)

- Choose your micro-investing platform

- Set up your first account

- Make your initial deposit (even if it’s just $5)

Week One Checklist

- Link your bank account and cards

- Set up round-ups

- Configure your first automatic deposit

- Choose your initial investment strategy

Month One Goals

- Review your round-up activity

- Make your first portfolio adjustment

- Track your investing patterns

- Plan your scaling strategy

Remember, every successful investor started somewhere. Your $5 investment today could be the first step toward significant wealth tomorrow. The key isn’t having a lot of money to invest – it’s starting early, staying consistent, and letting time work in your favour.

Ready to start your micro-investing journey? Scroll back up to the platform comparison section, choose your platform, and take that first step today. Your future self will thank you.